Blog

Six Important Action Points for 2025

Leigh Kent • 7 January 2025

Six steps to improve your financial efficiency and resilience in 2025

1. Review Regular Expenses

Spend some time reviewing your bank and credit card statements to identify unnecessary expenses. Review digital subscriptions and set reminders for deals coming to an end – watching out for car insurance renewals, mortgage rate changes, and ending mobile phone contracts can save you significant amounts.

2. Have a Cash/Investment Strategy

Do you have the right ratio between saving and investing? Experts suggest balancing cash reserves (for shorter-term needs) and long-term investments. Maintain a cash emergency fund (some suggest 3-6 months of living expenses, more if retired or self-employed) but can savings beyond this amount be used to invest toward your longer-term goal? Speak to us if you would like investment advice.

Utilize your spouse's tax allowances for savings and investments.

3. Inheritance Tax (IHT)

Defined contribution (DC) pensions will be included in IHT from April 2027 pushing up the potential Inheritance Tax liability of many. Update your beneficiaries' forms for your pensions. Consider strategies to minimize IHT and/or explore inheritance tax insurance. We are happy to provide independent advice on this often-complex area.

4. Tax Thresholds

Frozen tax thresholds are dragging more people into higher-rate tax brackets. Consider increasing pension contributions through salary sacrifice or opt to have bonuses paid into pensions. We are pleased to offer advice in this area.

Also explore employer schemes for purchasing or leasing electric vehicles and the Cycle to Work scheme.

5. Protection Insurance Review

Examine your Income Protection/Permanent Health Insurance cover. Some employers offer this as a benefit. Speak with your employer to verify what you already have and consider additional private cover to meet your basic monthly outgoings in the event of ill-health. We can help you understand what cover you need and scour the market for competitive premiums and the best terms.

Establishing a Lasting Power of Attorney (LPA) for health and finances can also be important in managing affairs during temporary incapacity.

6. Pension Check-Up

Check your state pension forecast on Gov.uk and consider whether you need to top up your National Insurance (NI) record before the April 2025 deadline. Review whether your retirement plan is broadly on track via our Retirement MOT service. See our website

for further details.

November’s Budget announced a range of changes to ISAs, the full extent of which did not become clear immediately. While the Office for Budget Responsibility (OBR) managed to publish its primary document before the Chancellor spoke, HMRC and the Treasury were slow in releasing information through to the end of Budget week. The main ISA details, as we now know them, are: The yearly subscription limits (£20,000 overall for an adult ISA, £9,000 for a Junior ISA and £4,000 for a Lifetime ISA) will be frozen until April 2031. The adult ISA limit was last increased in April 2017, meaning the freeze will last (at least) 14 years. From April 2027, the maximum subscription to a cash ISA will be £12,000 for under-65 year olds. Those aged 65 and over can still subscribe to their full £20,000 cash ISA allowance. Also from April 2027, there will be new restrictions on the funds that can be held in stocks and shares ISAs by the under-65s. These will be designed to exclude ‘cash-like’ funds, such as money market funds. It is unclear whether these restrictions will only apply to new subscriptions or also cover existing investments. When the new restrictions begin, any interest earned on cash held in stocks and shares ISAs by under-65s will be subject to a charge, currently unspecified. A consultation paper will be published soon on the design of a new ISA to support first-time buyers saving for a deposit. Once this new ISA becomes available, the Lifetime ISA (LISA) will be withdrawn. It is unclear whether subscriptions to existing LISAs will then have to stop, but precedent suggests otherwise. These changes are largely a reversion to the past ISA formats. The revised treatment of cash ISAs echoes the situation before July 2014, when the cash subscription limit was half of the overall maximum and interest received in a stocks and shares ISA suffered a 20% charge. Similarly, until December 2019 when it was replaced by the LISA, there was a Help to Buy ISA. As the tax year end approaches, if you are thinking of investing in an ISA, make sure you get advice about how the planned changes could affect your choice of plan. Notes: Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances. The value of the investment and the income from it can fall as well as rise and investors may not get back what they originally invested, even taking into account the tax benefits. Investors do not pay any personal tax on income or gains, but ISAs may pay unrecoverable tax on income from stocks and shares received by the ISA managers. Stocks and Shares ISAs invest in corporate bonds, stocks and shares and other assets that fluctuate in value. Tax treatment varies according to individual circumstances and is subject to change. The Financial Conduct Authority does not regulate tax advice.

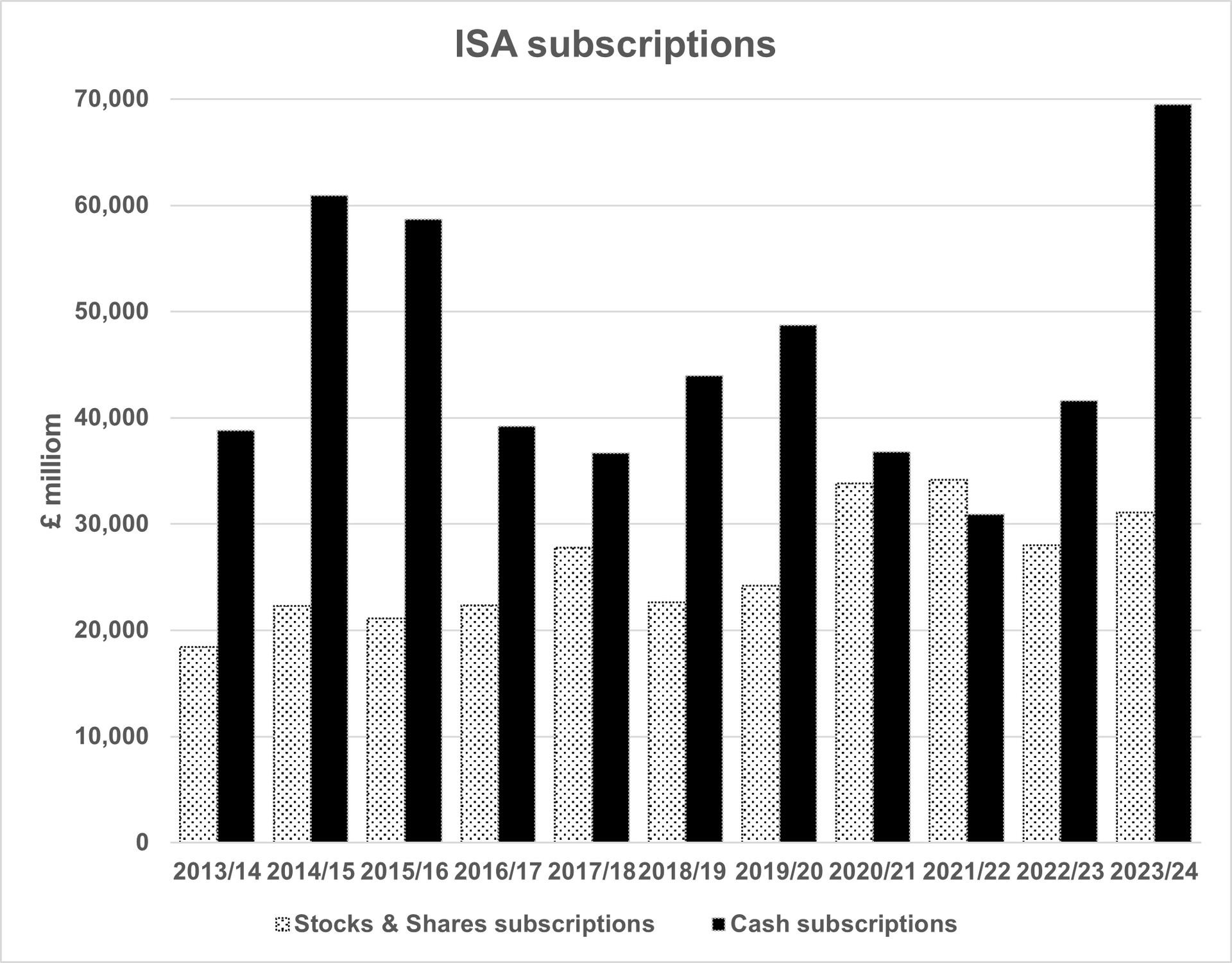

The Chancellor’s plan to reform individual savings accounts (ISAs) to “improve returns for savers” has been considered for some time. Rachel Reeves’s scheme is widely believed to mean the current £ 20,000-a-tax-year subscription limit for ISAs would be reduced for cash ISAs. Unsurprisingly, the investment management industry has been in favour of such a move, while the big banks and the Building Societies Association have been strongly against it. Statistics published by HMRC in September cast a new light on the ISA debate. The data (see chart below) show that in 2023/24, subscriptions to cash ISAs were £69.5 billion, while stocks and shares ISAs attracted just over £31 billion. That brought the total amount invested in cash ISAs to £360 billion as of April 2024. It would be reasonable to assume the total now is well above £400 billion. Now put yourself in the Chancellor’s shoes. If the Bank of England had £400 billion earnings and 4% Bank Rate, it would mean £16 billion of interest on which no income tax is being collected. The latest estimate from HMRC is that the cost of income tax and capital gains tax relief for ISAs was £9.4 billion in 2024/25, almost a fifth up on the previous year. Cutting back on the amount flowing into cash ISAs could reduce tax loss, even though the prospect of enhanced returns is a better story to present to the public. To be fair to the Chancellor, there is some justification in her argument. As HMRC’s ISA Investment values and subscriptions graph illustrates, to a degree, the total value of stocks and shares ISAs grew more rapidly than cash ISAs over the ten years to April 2024. However, cash ISAs saw little net inflow for much of the period. It is easy to forget now that the Bank of England rate was no more than 1% between February 2009 and June 2022, assuring miserable returns for money held on deposit. Before you rush to arrange a pre-Budget cash ISA, it is worth reflecting on what you are trying to achieve. If you just want to move a ready money deposit to a tax shelter, remember that unless you are an additional/top rate taxpayer, the personal savings allowance (PSA) covers up to £200 of tax on interest (20% for basic rate x £1,000 PSA or 40% higher rate x £500 PSA). If you are setting aside money for long-term growth, then, as the Chancellor suggests, there could be better options.

In early September, the Deputy Prime Minister (and Housing Secretary) resigned after discovering that she had underpaid SDLT by £40,000 on the purchase of a flat in Hove. That Rayner missed the history of the additional tax liability was unfortunately ironic. The surcharge on stamp duty was introduced by Conservative Chancellor, George Osborne, in the Autumn Statement 2015, at a rate of 3%. It took effect from April 2016 and the rate was subsequently increased to 5% nine years later in the Autumn Budget presented by Angela Rayner’s then cabinet colleague, Rachel Reeves. The tax aimed to discourage buy-to-let and second home purchasers, who were often shopping for similar properties to first-time buyers in a pressured housing market. The basis of the additional tax required the buyer to pay extra SDLT if they owned another residential property on the same day that another property was bought. That might sound simple enough, but the legislation to achieve it was not, involving the closure of potential loopholes, such as buying the second property through a company or using trusts to shift ownership. It was the latter anti-avoidance measure which tripped up Angela Rayner. She had sold the 25% interest in her first home, in Ashton-under-Lyne, to a trust for the benefit of her disabled child before buying her Hove apartment. Paragraph 12 of Schedule 4ZA of the Finance Act 2003 deemed that such a sale meant that Rayner was still treated as owning the property for SDLT purposes. While Rayner had sought guidance on her SDLT position, the advice she received was qualified by the acknowledgement that it did not constitute expert tax advice and was accompanied by a suggestion, or in one case a recommendation, that specific tax advice be obtained. Had Rayner paid heed to those warnings, she would not now be facing a potential tax penalty of up to £12,000 for ‘carelessness’, in addition to the £40,000 extra SDLT. The lesson of the whole episode and one to keep in mind whenever advice – particularly in the financial area – is needed: make sure you are talking to an expert who stands behind their judgement. The Financial Conduct Authority does not regulate tax advice.

Recent statistics issued by HMRC show that company car ownership (the top line) is enjoying a revival after a 25% fall between 2015/16 and 2020/21. The reason for the increase is largely explained by the second line, which shows electric company car ownership. As recently as 2018/19, less than one company car in two hundred was a zero-emission vehicle: By 2023/24 (the latest data), the proportion had changed to about two in every five. Over the same period, the diesel share of the company car population dropped from over two in three to just one in eight. The switch to green does not signify that company car drivers are becoming environmentalists over the decade. Instead, it is a clear demonstration of how tax changes can drive behavioural change: In April 2017, HMRC introduced a new approach to taxing company cars that were provided under salary sacrifice or similar arrangements. In many instances, the new regime, called Optional Remuneration Arrangement (OpRA), made salary sacrifice less attractive because it ended up basing the personal tax on the company car regime rather than, as previously, the amount of salary foregone. To encourage take-up of low-emission cars, an exclusion was carved out for cars with CO2 emissions of up to 75g/km (of which there were very few at the time). In 2020/21, the benefit-in-kind percentage charge on zero-emission cars was cut from 16% to 0%. Thereafter, for the next two years, it rose by 1% a year, reaching 2% in 2022/23 and staying at that level until a further 1% rise to 3% for the current tax year, 2025/26. In contrast, a petrol car with 100g/km of CO2 emissions saw its scale percentage rise marginally from 24% in 2019/20 to 25% currently. The combination of inducements has proved almost too successful: the total taxable value of all company cars fell from £5.43 billion in 2019/20 to £3.27 billion in 2023/24. Now, however, the percentage scale charge for zero-emission cars is on the increase and by 2029/30, it will be 9% – three times the current level. It may still be worth considering salary sacrifice for an electric company car, but the tax calculations will not be as favourable. Tax treatment varies according to individual circumstances and is subject to change. The Financial Conduct Authority does not regulate tax advice.

On Friday 2 May the news was full of stories about the results of the previous day's local election results and the first by-election of the current Parliament. There was little other news coverage – give or take an interview with Prince Harry. There was, however, a story that got too little attention… The Department for Health and Social Care (DHSC) chose Friday 2 May to publish the terms of reference for its independent commission into adult social care in England. The commission was first announced in early January 2025, to be headed by Baroness Louise Casey. Its launch followed Rachel Reeves’ decision in July 2024 to abandon her predecessor’s plan to cap fees for social care in England from October 2025. This scheme had already been deferred several times since its framework was set up by the Care Act 2014. The Chancellor’s cull almost went unnoticed while focus remained on her scrapping of the universal Winter Fuel Allowance. However, the consequences were brought into stark contrast by the release of the Casey commission’s terms of reference on 2 May. This confirmed that the commission would have two separate phases: Phase 1 (medium term) This phase “…set out the plan for how to implement a national care service”. In a fine piece of Whitehall speak, the terms require that “The commission’s work on medium-term reform will be a data-driven deep-dive into the current system”. Given the number of inquiries, reviews and even a Royal Commission that has examined the subject over the years, it is hard to imagine any significant new insights emerging. Nevertheless, the commission will have until 2026 to report. Phase 2 (long term) This second two-year phase will look at “…how services must be organised…and discuss alternative models that could be considered in future to deliver a fair and affordable adult care system”. In other words, it will consider the question that has stymied every proposal to date – how to pay for care. How long before a new system arrives? The possible answer may well lie in that choice of publication date: “The commission should produce tangible, pragmatic recommendations that can be implemented in a phased way over a decade”, which means by 2036. Meanwhile, the upper capital limit for English local authority funding support remains at £23,250, where it has been since April 2010. With no clear timeline for adult social care reform, care costs could remain a significant consideration for individuals in long-term financial planning.

Changes to State Pension Age (SPA) have proved fertile grounds for controversy. The move to equalise women’s and men’s SPA at 65, completed in November 2018, is still a source of dispute. In March 2024, the Parliamentary and Health Service Ombudsman (PHSO) published a report recommending that the women affected by that change should each receive up to £3,000 compensation. A couple of days before parliament rose for its Christmas 2024 recess, the government announced that it disagreed with the PHSO and would not be following its recommendations. Despite members of the government having sounded much more supportive of the affected women while on the opposition benches, the move was no surprise given that the suggested compensation would involve a potential bill of up to £10.5 billion. The PHSO argued that past governments had not communicated clearly enough to inform the affected women about their SPA changes. This lack of clear information occurred even though the equalisation of SPA was initially made law in 1995 (with a final target of April 2020). That date was moved earlier to November 2018 by new laws in 2011, which also brought in another SPA increase to 66 by October 2020. Next change on the horizon The phasing in of the next SPA increase to 67 starts in less than a year and ends in April 2028. You might have thought that the protracted debate and well-publicised legal arguments about equalisation means that those affected (anyone born after 6 April 1960) know about the change. However, recent research by the Institute for Fiscal Studies (IFS) revealed that many people are still unaware. The IFS found that among people born between 1955 and 1965 who were interviewed between 2021 and 2023 as part of a long-term study of ageing, 40% were unclear on their position: • 60% knew their SPA to an accuracy of within three months. • 18% overestimated their SPA, expecting it to be higher than legislated. • 11% underestimated their SPA. • 11% fell into the ‘Don’t know’ category. As the IFS noted, “Knowing one’s state pension age is crucial for financial and retirement planning.” After all, for current pensioners, on average, the State Pension makes up about 44% of overall income, according to the IFS. Which category do you fall into? If you want to prove yourself right – or wrong – on your SPA, check at: https://www.gov.uk/state-pension-age .

It’s been five years since the pandemic turned the world upside down. The experience provided lessons in many aspects of life, not least its potential fragility. During the lockdowns, many people became suddenly aware that they had no will or, if they did, it was woefully out of date. The realisation came at a time when making an appointment with a solicitor or will-writer was nearly impossible because of the restrictions imposed on movement and meeting. Half a decade later, were a new pandemic to arrive, such as a mutant bird flu, are you sure that your will is up to date? If you cannot answer yes, then you know, for your family’s sake, what you need to do. However, whether or not you have made sure your will is up to date, it is best thought of as a starting point rather than the end of the matter. To be able to follow your will’s instructions, for all but the smallest estates, the people you have chosen as your executors must first obtain a grant of probate (confirmation in Scotland). In turn, this will require them to calculate the net value of your estate. This is often the point at which executors begin to realise the task they have taken on. Accessing records Imagine that your estate was the one to be valued: how easy would it be for your executors to prepare a list of what you owned and what you owed? Initially, they might ask a surviving spouse or partner – if one exists – for details. Unfortunately, that can sometimes produce a response such as, “Sorry, I always left money matters to him/her”. What your executors would hope to find is a reasonably up-to-date list of your investments, bank accounts, pensions and other assets, including any borrowing (for example: credit cards, personal loans and mortgages). Ideally, each item on the list would have the relevant account/customer numbers and contact details. If you haven’t already set up such a document – on paper or an accessible digital form – your executors are not the only ones facing a struggle. You may be, too, trying to manage your finances, especially as you get older. Taking the time to organise your affairs now, while you can, could be one of your greatest gifts to those you will leave behind. The Financial Conduct Authority does not regulate wills and will writing.

The Chancellor has announced the timing of her next formal report to Parliament.

In the first month of 2025, online trading platforms such as eBay, Airbnb and Vinted had to provide HMRC with a report on their users’ sales in 2024. This was the first time such reporting had been due, although the origins of the requirement date back to 2020 when the Organisation for Economic Co-operation and Development (OECD) published model rules targeted at tax avoidance via digital platforms. When it first emerged that HMRC would be sent this information there was a flurry of inaccurate media coverage with scare-mongering headlines such as ‘eBayers to be taxed’. In response, HMRC issued a press release before Christmas with the straightforward headline, ‘No tax changes for online sellers’. While ‘no change’ is factually correct, it may feel like a change for those questioned by HMRC on their selling activities. With this in mind, it is important to understand the rules. HMRC will only receive a report from a platform if, in 2024, the individual: • Had sales of at least €2,000 (about £1,700); or • Made at least 30 sales. The reports have nothing directly to do with personal tax liability, although they will encourage HMRC to raise queries about whether one exists. If all you are doing is selling your unwanted items online, that is not a taxable activity. What HMRC wants to know about is people who are: • Trading, i.e. buying items for resale at a profit; or • Providing services, be that driving a van or letting out a property. These activities have always been taxable – hence HMRC’s “no change” stance. However, even if you do have trading or rental income, you will not have any tax liability if: • Your total gross trading/services profit (i.e. before deducting any expenses) is not more than £1,000 in a tax year; and/or • Your total rental income (again before expenses) is similarly no more than £1,000 in a tax year. These £1,000 annual trading and property allowances are little known and are as much about saving HMRC administrative hassle as helping their ‘customers’. As ever in tax, the finer the detail, the more useful understanding it can be. Tax treatment varies according to individual circumstances and is subject to change. The Financial Conduct Authority does not regulate tax advice.

It is the turn of the year. The health secretary of the relatively new Labour government announces a commission to review the financing for long-term care of the elderly. Can you name the year? You may not be surprised to know that there are two correct answers: 1997: in December of this year, Frank Dobson, the Health Secretary in Tony Blair’s new government, fired the starting gun for a Royal Commission report with the title "With Respect to Old Age: Long Term Care – Rights and Responsibilities." The report was published in March 1999 and its main recommendation – that the state should pay for personal care – was rejected by the government in July 2000 2025: in January of this year, Wes Streeting, the Secretary of State for Health and Social Care in Sir Kier Starmer’s government, said he would be launching an independent commission into adult social care. An interim report is due in 2026 which “will identify the critical issues facing adult social care and set out recommendations for effective reform and improvement in the medium term”. The commission’s final report which, among other elements, consider “how to best create a fair and affordable adult social care system for all” is due by 2028. Between 1997 and 2025, there were numerous other commissions, white papers, inquiries and reviews. These have mainly focused on England, as from the late 1990s social care became the responsibility of devolved governments. Nevertheless, the four countries’ long-term care funding rules all have a similar structure and rely in some part on means-testing above relatively modest thresholds. For example, in England an individual with capital of over £23,250 is responsible for the full cost of their care. England had been due to have a new care-funding scheme with a fee cap of £86,000 from October 2023. However, this was deferred until 2025 by the previous Chancellor and then abandoned by the current Chancellor last July on the grounds that the funding did not exist. Given that the next election is due by mid-2029, it seems unlikely that any reforms to care funding in England will be legislated for until the next decade. If you are concerned about how you will need to fund your or a loved one’s long-term care, early planning is the first step.